We’ve got a full month of 2025 behind us, and now we’re starting to get earnings data from the final quarter of calendar year 2024. So far, that data is unsurprising – the results are not straying too far, up or down, from expectations. But this week we’ll have some big names reporting, as Alphabet (NASDAQ:GOOGL) and Amazon (NASDAQ:AMZN) release their quarterly results.

Maximize Your Portfolio with Data Driven Insights:

- Leverage the power of TipRanks' Smart Score, a data-driven tool to help you uncover top performing stocks and make informed investment decisions.

- Monitor your stock picks and compare them to top Wall Street Analysts' recommendations with Your Smart Portfolio

These two mega-cap internet stocks dominate their respective niches – e-commerce and online search – and have leveraged that dominance to bring long-term success. Both companies also are proving adept at adapting to the changing tech environment, making advances in cloud computing and AI. They aren’t just jumping on those bandwagons – they are staking leadership positions.

Covering both Alphabet and Amazon for JPMorgan, 5-star analyst Doug Anmuth picks them out as the best internet stock to buy, ahead of the earnings calls. Anmuth, who is rated by TipRanks in the top 1% of the Street’s analysts, says of the internet stock sector generally.

“We remain positive overall on the Internet sector heading into 4Q24 earnings as we expect strong underlying results, but we recognize outlooks will be more mixed due to tougher 1Q comps, FX headwinds, & growth generally decelerating from last year’s high levels,” Anmuth noted.

We’ve used the TipRanks platform to look up the broader Wall Street view on both of these ‘Magnificent 7’ stalwarts; let’s give them a closer look, using the latest data and Anmuth’s comments.

Alphabet

We’ll start with Alphabet, the parent company of the internet’s two leading search platforms, Google and YouTube. Google, of course, is the premier online search engine; YouTube, while best known as a video hosting and posting platform, is also a leading search engine for video content. Through these two subsidiaries, Alphabet leads the market in online search – and has built up a vast storehouse of data on internet users, search habits, and website traffic preferences. This sort of data is a valuable raw material in the digital world, with applications in online advertising and in AI.

Unsurprisingly, Alphabet makes most of its money from online advertising revenues. In 3Q24, the company’s Google advertising segment generated over $65.8 billion in revenue, or 75% of the quarter’s $88.2 billion total top line.

Alphabet, in its earlier guise as Google, was an early adopter of AI technology. Google began using AI for autocorrect more than 20 years ago, and for online translations in 2006. Both Google and YouTube use AI to improve search results, offer suggestions to users, and to enable precise targeting of online ads. More recently, Alphabet has been using AI to power large language models (LLMs) that allow online translations to operate with greater accuracy – an important point for a company that conducts business globally, in local languages.

But the biggest AI news from Alphabet recently has been the launch of the company’s customer-facing generative AI platform, Gemini. The platform is designed to handle such issues as language translations and computer coding, and Alphabet is working to integrate Gemini into all of its online products – but it’s putting a special emphasis on working Gemini into the Android operating system for smartphones. The aim there is to put a viable AI assistant literally in the palm of the customer’s hand – where it can act as an immediate upgrade to smartphone and tablet applications.

We have already noted Alphabet’s 3Q24 results. The company is set to release its 4Q24 – and full-year 2024 – results today after market close. Revenues are predicted in the neighborhood of $96 billion, with an EPS of $2.13. We should note here that Alphabet began paying out dividends last year, and this past December made its third common share dividend payment. The 20-cent dividend annualizes to 80 cents per share and gives a modest forward yield – only 0.4%. The key here is that Alphabet has more than $93 billion in cash on hand, and can easily maintain and increase the dividend going forward.

Long story short, the prospects for Alphabet’s continued growth, and for its continued ability to provide returns to investors, are strong – and that is where JPM’s Anmuth starts with his summary of the company.

“We believe GOOGL sentiment is improving, with investors positive around Google’s tech advancements & GenAI innovations, coupled with continued optimism for further margin expansion & increased capital returns. The DOJ search distribution trial remains an overhang, but we believe the Street sees potential for a relatively more favorable outcome under the incoming administration. Our 4Q checks have been constructive on Search & YouTube ads — which should both benefit from strong holiday retail — and Google Cloud, with an accelerating pace of innovation setting up Google for a strong 2025… In our recent survey of almost 100 investors, which skewed toward long-only, Google ranked as the best performing Internet Mag 7 stock & best performing advertising stock for 2025,” Anmuth opined.

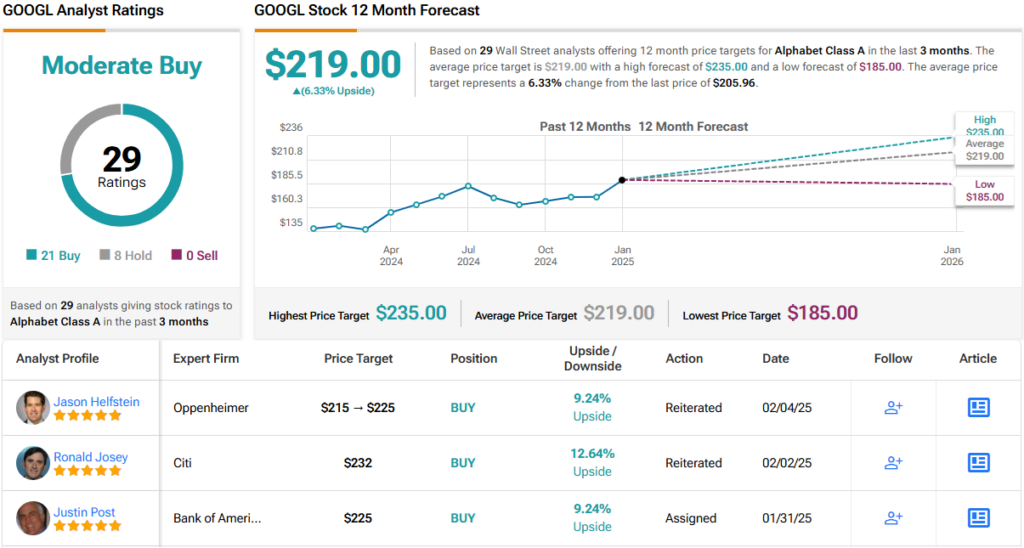

Anmuth quantifies his stance on GOOGL with an Overweight (i.e., Buy) rating, and a $232 price target that suggests he sees a ~13% upside potential for the stock this year.

Overall, there are 29 recent analyst reviews of GOOGL shares, and the 21 to 8 split favors Buys over the Holds for a Moderate Buy consensus rating. The stock is trading for $205.80 and holds a $219 average price target, implying a potential gain of ~6% on the one-year horizon. (See GOOGL stock forecast)

Amazon

Next on the list is Amazon, the world’s largest online retailer – and a leader in the fields of AI services and cloud computing. The company has leveraged its dominance of e-commerce to become a multi-trillion dollar behemoth on Wall Street – Amazon’s $2.5 trillion market cap makes it the fifth largest publicly traded firm in the US markets, and one of just nine valued at $1 trillion or more.

In the four quarters that ended with 3Q24, its last reported, Amazon generated a total of $620 billion in revenues, primarily through its core business of online retail. A look at its third-quarter numbers will tell the story. Total online commerce revenues in 3Q24 came to $131.4 billion; of that, $95.5 billion came from North America and $35.9 billion came from international sales. The company’s fastest-growing segment, however, was AWS, its cloud computing service. AWS revenues in Q3 came to $27.5 billion, up 19% year-over-year, outpacing the growth in Q3’s total revenue, which at $158.9 billion was up 11% year-over-year.

Amazon hasn’t sat on those laurels. The company’s success has allowed it to accumulate a reserve of $78.7 billion in cash and liquid assets, as of the end of 3Q24 – a reserve that gives the company the deep pockets needed to keep up with advances in consumer technologies, particularly cloud computing and AI.

Amazon has been integrating AI technologies into its retail operations, improving the customer interfaces on the website as well as targeted advertising. Among the additions are an AI-powered shopping assistant to improve the site search functions, allowing customers to find exactly the product and price points they are looking for. In addition, Amazon’s AWS cloud platform now includes an array of AI tools, and Amazon has been working on its own AI platform, Bedrock, to build generative AI models. The Bedrock project is proceeding in partnership with the AI development company Anthropic. Amazon is even working to develop a line of AI-capable semiconductor chips, under the Trainium name, purpose-built for training and expanding AI and natural language processing systems.

What all of this means is that Amazon is more than just an online retailer. The company has recognized the leading trends in consumer tech – and is adapting those technologies to bring in new customers. While online retail is currently Amazon’s bread and butter, the company has charted a long-term course based on cloud computing and AI.

This makes Amazon hugely profitable. Earnings per share in 3Q24 came to $1.43, beating the forecast by 29 cents per share. Looking ahead, the company has scheduled its release of 4Q and full-year 2024 results for February 6 after the markets close. The Street’s analysts are expecting to see Q4 EPS at or near $1.49, and total quarterly revenues to the north of $187 billion.

A solid position and strong prospects for continued growth are powerful assets for any investment and make up the core of Doug Anmuth’s take on Amazon. Writing up the JPM view of this market leader, Anmuth says, “We believe AMZN is well-owned and a top pick for many… Secular growth, new workloads, & growing GenAI contribution drive AWS growth acceleration & 20%+ growth in ‘25, & we came away from re: Invent believing that AWS is tightening the GenAI gap through its full-stack approach. We project 6.6% N. America OI margin expansion in 2025 (+64bps Y/Y) driven by inbound regionalization & inventory placement, SD facility buildout, & automation/ robotics. We model FCF of $64B in ‘25 (+37% Y/Y), reflecting strong growth even against our projected $97B ‘25 capex (+29% Y/Y), and we believe capital returns are possible in 2025. We believe investors are looking for 4Q Net Sales of $188B-$189B, AWS growth of 20%+, & OI of $19B-$20B+. We believe valuation is attractive w/shares trading at ~26.5x 2026E FCF…”

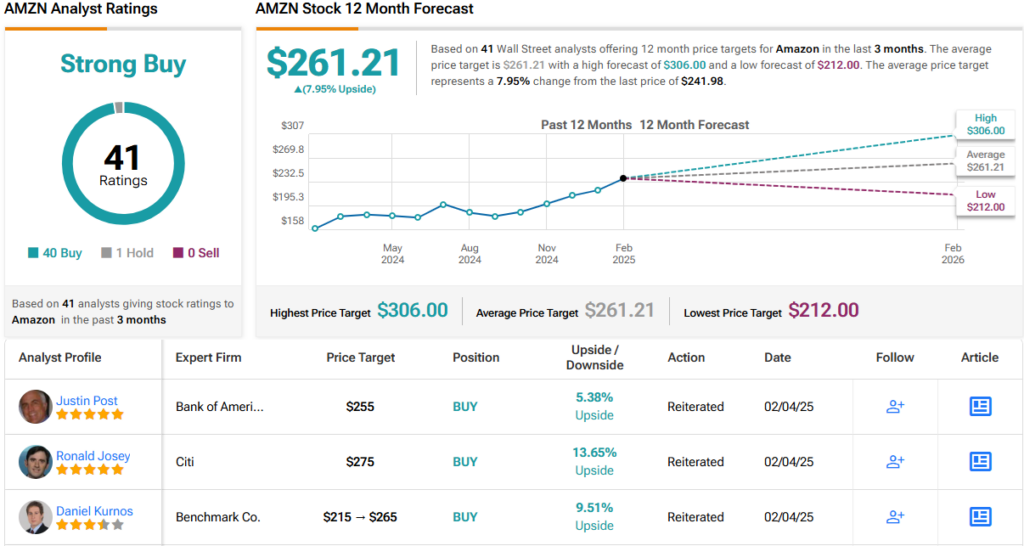

Anmuth goes on to rate AMZN shares as Overweight (i.e., Buy), with a $280 price target that points toward a one-year gain for the stock of ~16%. (To watch Anmuth’s track record, click here)

Overall, Amazon has picked up no fewer than 41 analyst reviews – and these include a lopsided split of 40 Buys to 1 Hold, for a Strong Buy consensus rating. The shares are currently priced at $241.97, and their average price target of $261.21 implies a 12-month upside potential of ~8%. (See AMZN stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.