Ally Financial reported Friday that adjusted earnings per share rose 24% in 3Q year-on-year to $1.25 per share, beating analysts’ estimates of $0.68. Its revenues rose 4% to $1.68 billion compared with the Street consensus of $1.55 billion. Shares rose 2.7% on Friday.

Invest with Confidence:

- Follow TipRanks' Top Wall Street Analysts to uncover their success rate and average return.

- Join thousands of data-driven investors – Build your Smart Portfolio for personalized insights.

Ally Financial’s (ALLY) CEO Jeffrey Brown said that the 3Q results “reflect ongoing strength in credit performance, focused execution from our leading auto finance and deposits businesses, as well as ongoing momentum from our expanded consumer offerings.”

Excluding Core OIDB (Original Issue Discount Balance), net interest margin (NIM) was 2.67% in 3Q, down 5 basis points from the year-ago period. The company said net interest margin declined due to “elevated liquidity levels and mortgage premium amortization more than offsetting higher gains on off-lease vehicles, retail auto portfolio yield expansion and lower funding costs.” (See ALLY stock analysis on TipRanks).

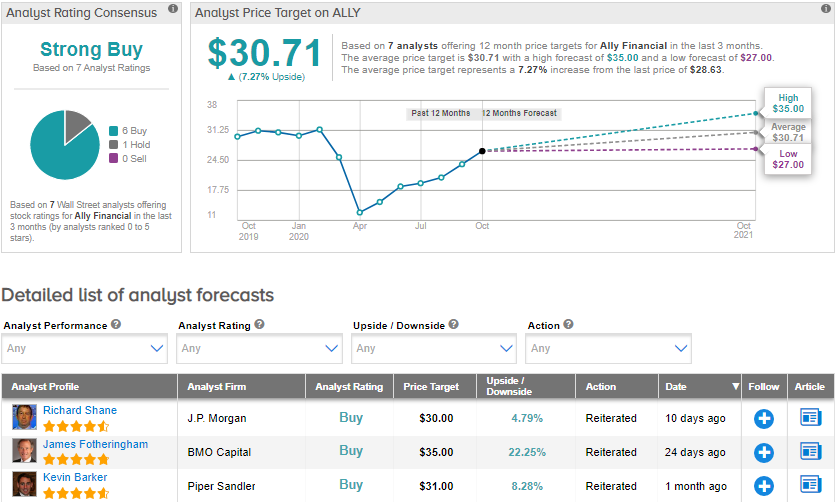

On Sept. 25, BMO Capital analyst James Fotheringham maintained a Buy rating on the stock and a price target of $35 (22.3% upside potential). The analyst had anticipated net interest income to see “material growth” in 3Q20, as NIM rebounds and expands about 25 basis points from the preceding quarter. The analyst also raised his 2020 EPS estimate by 25% but reduced his 2021 EPS estimates by 5% (to $4.08 from $4.27), and by 4% in 2022 (to $5.09 from $5.29) on higher expense growth expectations.

Currently, the Street is bullish on the stock. The Strong Buy analyst consensus is based on 6 Buys and 1 Hold. The average price target of $30.71 implies upside potential of about 7.3% to current levels. Shares are down by about 6.3% year-to-date.

Related News:

Kansas City Misses 3Q Sales Est.; Shares Drop

Cars.com Soars 26% On Strong 3Q Sales Outlook, Analyst Upgrade

VF Tops 2Q Estimates; Shares Decline