Advanced Micro Devices (NASDAQ:AMD) may still have a shot at catching up to Nvidia (NASDAQ:NVDA) – at least in terms of stock returns, if not market share.

Nvidia has dominated the market for semiconductor chips designed for artificial intelligence, with estimates placing its share between 70% and as high as 95%. This dominance has played a key role in Nvidia’s stock soaring 168% over the past 52 weeks. However, Bank of America analyst Vivek Arya suggests that AMD, Nvidia’s long-standing rival, might still have a chance to close the gap.

And that chance comes on October 10.

In a recent research note, Arya describes the opportunity. October 10 is the date of AMD’s upcoming Advancing AI event, you see, and, as the analyst points out, the last time this event rolled around, the announcements AMD made helped push the stock up 19% over the ensuing month – and up 80% over the next three months.

Now, what will AMD have to tell investors this time to achieve a similar result?

As Arya points out, expectations for AMD are already high, with analysts on average anticipating that AMD will reach $5 billion or more in AI sales by the end of this calendar year, and nearly double that number in 2025. These expectations are based on a belief that AMD will retain no more than its current 5% to 7% market share in AI chips, “well below its 20%+ share in consumer CPU and gaming GPU.”

But what if AMD promises next week to grow its market share to 10% – twice what most analysts think it can achieve?

Arya argues there’s a “credible” path to AMD hitting a 10% market share – if not this year or next, then at least by 2026. And if AMD does that, then this could add an additional $5 billion to the $12.6 billion in 2026 AI sales that analysts are already expecting. Such a result – 40% better sales than expected – would naturally have a positive effect on the stock price.

There are, however, caveats. In musing over the potential for a 10% market share, Arya suggests AMD might also earn as much as $8 or $9 per share. But here’s the thing: Analysts positing the more likely scenario of 5% to 7% market share think that alone would earn AMD $7.37 per share. Even at the upper range of Arya’s forecast (i.e. $9 a share), though, this would represent earnings only 22% above the consensus forecast.

Translation: For AMD to deliver sales 40% better than expected, it’s probably going to have to fight a price war against Nvidia, and accept lower prices for its chips – low enough that profits will grow much slower than sales.

That doesn’t sound like a great business strategy, but in Arya’s opinion, it might still make for a successful AMD stock. 40% better than expected sales growth, argues the analyst, could help AMD stock “rerate” towards the 30-55x forward PE ratio that investors awarded the stock during its last big growth spurt (from 2019 through 2022), as investors reward the stock for sales growth and market share gains, and overlook any profit margin shrinkage necessary to achieve these goals.

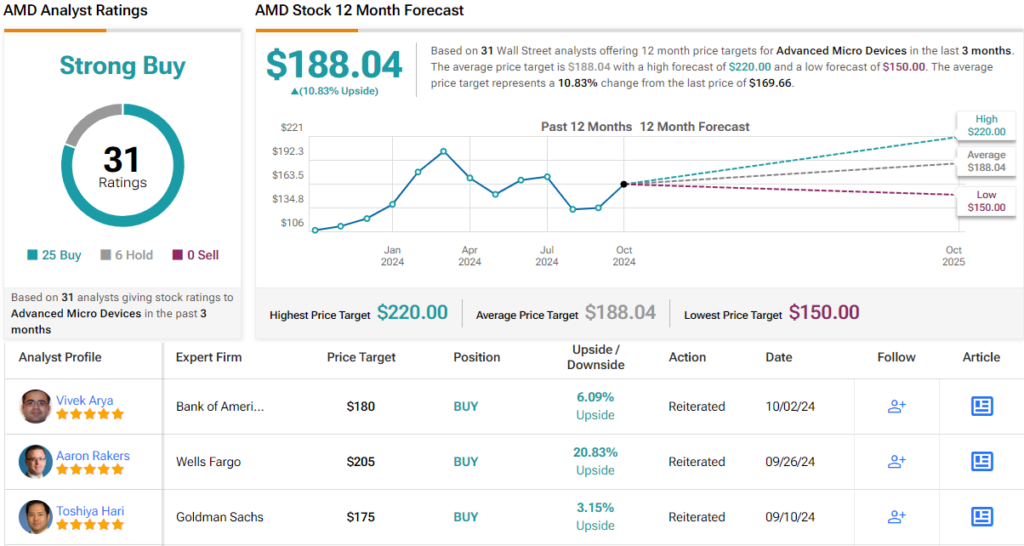

Just the chance of that happening has this analyst recommending AMD as a “buy,” and maintaining his price target of $180 a share on the stock. (To watch Arya’s track record, click here)

Not many are arguing with that take on Wall Street. AMD’s Strong Buy consensus rating is based on 25 Buy recommendations and 6 Holds. The forecast calls for one-year gains of ~11%, considering the average price target stands at $188.04. (See AMD stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.

Questions or Comments about the article? Write to editor@tipranks.com