Sometimes, it’s hard to ignore the haters and concentrate on what’s important. Yet, this is a crucial skill for all investors to have. Alibaba (BABA) is a perfect example, as the company’s latest round of results certainly isn’t perfect, but Alibaba has strong points you won’t want to overlook. Hence, I am bullish on BABA stock because the company is doing well financially, given the challenging circumstances in China.

Alibaba is a China-based e-commerce and delivery company that’s similar to Amazon (AMZN) in the U.S. Let’s not forget that Alibaba has to operate under difference circumstances than Amazon. China is dealing with a stagnant economy after easing COVID-19 lockdowns in late 2022, as well as an ongoing crisis in the nation’s property market.

After glancing through the self-appointed gurus on social media, I get the impression that some U.S. traders have the same expectations for Alibaba that they have for Amazon, which is unfair. Instead of paying attention to the haters and naysayers on social media, investors can check the actual facts while also considering the consensus assessments of well-respected analysts on Wall Street. Now, that’s what I would call a smart approach to investing in Alibaba.

Alibaba: First, The Bad News

I’ll just come out and say it: Alibaba’s bottom-line results for the second quarter of 2024 weren’t great. In particular, the company’s income from operations declined 15% year-over-year to $4.952 billion (all dollar figures will be translated from China’s RMB currency). Even worse, Alibaba’s net income dropped 27% to $3.306 billion. So far, not so good.

The fall-off isn’t quite as drastic when we look at Alibaba’s Q2-2024 adjusted (non-GAAP) earnings of $2.26 per ADS (American depository share), down 5% year-over-year. Another bottom-line metric, adjusted (non-GAAP) EBITA (not to be confused with “EBITDA,” which includes a “D” for “depreciation”), only declined by 1% year-over-year to $6.197 billion for Alibaba. However, I’m probably grasping at straws for positive-sounding results now.

On the other hand, The Wall Street Journal (WSJ) offered a tidbit that should offer hope for the bulls. The WSJ noted that while Alibaba’s adjusted net profit fell 9.4% to 40.69 billion yuan, this result topped analysts’ consensus expectation of 37.88 billion yuan. That’s got to be worth something, right?

Still, Alibaba’s press release didn’t really explain why the company’s net income decreased so much. The WSJ clarified that Alibaba’s “bottom line was hurt by higher expenses for marketing, product development and general and administrative costs, as well as a jump in taxes.” Going forward, investors should monitor Alibaba’s spending habits to make sure they don’t get completely out of control.

Don’t Just Overlook Alibaba’s Positive Points

To paint a positive picture, you can’t just disregard Alibaba’s strengths in 2024’s second quarter. That’s a mistake that the haters on social media make, but you can be smarter and potentially more profitable when it comes to Alibaba stock.

One notable highlight was Alibaba’s Cloud Intelligence Group revenue, which grew 6% year-over-year. This result was, according to Alibaba, “driven by double-digit public cloud growth and increasing adoption of AI-related products.”

Speaking of AI-related products, the number of paying users using Alibaba Cloud’s AI platform surged by over 200% in Q2 2024 compared to Q1 2024. This magnitude of growth reminds me of Amazon, which is a cloud contender as well as an e-commerce giant.

Sticking to the topic of technology and e-commerce, Alibaba’s International Digital Commerce Group revenue grew 32% year-over-year to $4.031 million. It sounds like Alibaba could have turned a decent profit in Q2 2024 if the company hadn’t spent so much capital on marketing, product development, and so on. It remains to be seen whether all of those capital outlays will pay off in the long run.

Finally, the haters and doubters can’t deny Alibaba’s penchant for share buybacks. In 2024’s second quarter, the company repurchased a whopping 613 million ordinary shares for a total of $5.8 billion.

Why is this relevant? It’s because share buybacks can reduce the supply of available shares, and a lower supply could potentially boost the share price. Alibaba observed that, as of June 30, 2024, the company had 19,024 million ordinary shares outstanding, representing a net decrease of 445 million ordinary shares when compared to the share count from March 31, 2024.

Is Alibaba Stock a Buy, According to Analysts?

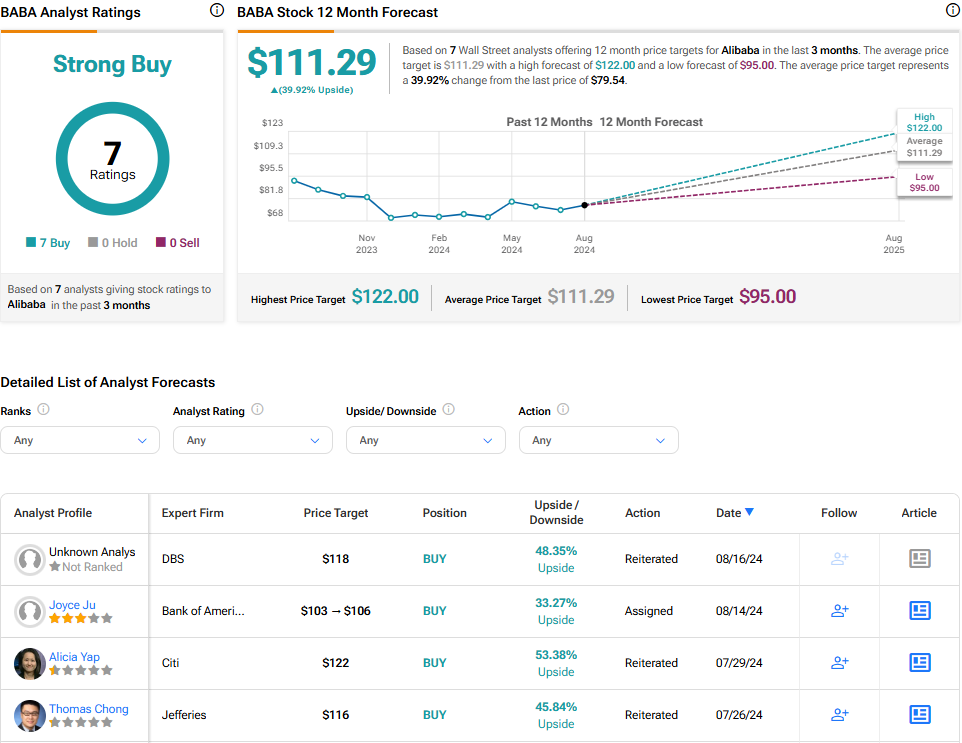

On TipRanks, BABA comes in as a Strong Buy based on seven unanimous Buy ratings assigned by analysts in the past three months. The average Alibaba stock price target is $111.29, implying 39.9% upside potential.

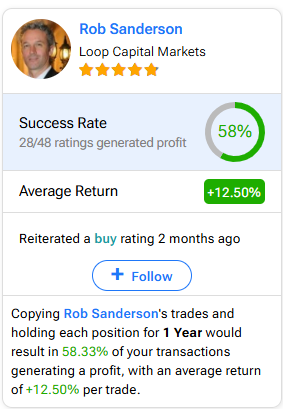

If you’re wondering which analyst you should follow if you want to buy and sell BABA stock, the most profitable analyst covering the stock (on a one-year timeframe) is Rob Sanderson of Loop Capital Markets, with an average return of 12.5% per rating and a 58% success rate. Click on the image below to learn more.

Conclusion: Should You Consider Alibaba Stock?

The market was ho-hum about Alibaba stock after the company released its quarterly results. The stock didn’t move much, possibly because the market was busy weighing the firm’s mixed bag of results.

Yet, I expect the market to appreciate Alibaba’s positive points in the long run. I encourage you to revisit Alibaba’s results, especially concerning the company’s Cloud AI platform and International Digital Commerce Group.

Then, take note of Alibaba’s large-scale share repurchases. With all of that in mind, I would keep the haters at a distance and consider buying BABA stock now.