Airbnb, Inc. (ABNB), a leading global vacation rental platform, has seen its stock price fall marginally this year amid the waning of the post-Covid travel boom. However, the company is well-positioned to benefit from Fed rate cuts as an increase in consumers’ disposable income is likely to keep travel demand robust for the foreseeable future. I am bullish on Airbnb stock, as I believe the company has a long runway to grow by taking market share from traditional travel booking platforms such as Booking Holdings, Inc. (BKNG).

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

The Long-Term Macroeconomic Outlook is Positive

One of the main reasons behind my bullish stance on Airbnb is the favorable long-term industry outlook. Airbnb’s year-over-year revenue growth decelerated to just 10.6% in the second quarter, well below the highs of 20%+ registered during the initial stages of the post-pandemic era. This slowdown in growth is a direct result of the waning impact of the post-Covid travel boom. However, Fed rate cuts should boost the disposable income of consumers, resulting in increased travel spending in 2025. According to CBRE Group, revenue per available room in the U.S. is expected to grow from 0.5% in H1 2024 to 2% in the second half of the year. This is a clear indication that travel demand is picking up amid rate cuts and cooling inflation.

The increased work flexibility offered by large-scale employers is another main reason behind the promising outlook for the travel sector. According to an Upwork study, 22% of the American workforce will be remote by 2025, which represents more than 36 million Americans. The rising popularity of hybrid and flexible work arrangements should boost the demand for travel and leisure in the long term as people are less bound to a specific physical location.

The notable rise of experiential travel is another favorable macroeconomic development that tilts the odds in favor of Airbnb. Experiential travel has expanded the horizons of travelers by paving the way for more authentic interactions with their selected destinations. With this, travelers are no longer just looking for accommodation options but also for localized experiences. According to Skift data, the experiential travel market will see revenue of $3.1 trillion in 2025.

Airbnb is Expanding its Reach

In addition to the favorable long-term outlook enjoyed by Airbnb, I am impressed by the company’s recent initiatives to expand its addressable market opportunity. During the second-quarter earnings call in August, CEO Brian Chesky revealed that a new co-hosting marketplace is scheduled to be launched in October. This marketplace will match people who own properties with experienced Airbnb hosts who are looking for additional properties to manage. This novel concept should meaningfully expand the inventory levels of Airbnb, giving more options for travelers.

Moreover, the company is relaunching its experiences business in the coming months after refreshing the catalog to include more affordable, personalized, and localized experiences for travelers. In an interesting development, Airbnb is now focused on offering experiences that are unique to its platform, potentially paving the way to enjoy long-lasting competitive advantages. CEO Chesky also hinted in August that Airbnb will enter a transformative phase early next year as the company embraces long-term stays and guest services to diversify its business from short-term rentals.

Airbnb’s international expansion is also unlocking new growth opportunities for the company in underpenetrated markets such as Brazil, Germany, South Korea, and Switzerland. In Q2, Latin America and Asia Pacific led the way in driving nights and experiences booked to a record second-quarter high of 125.1 million. Airbnb is enjoying a first-mover advantage in some of these key regional markets, which is likely to result in competitive advantages.

Is Airbnb a Buy, According to Wall Street Analysts?

Although Airbnb is disrupting the travel booking industry, some Wall Street analysts believe the short-term will be challenging. For instance, Argus Research analyst John Staszak believes Airbnb’s earnings growth will come under pressure in the next few quarters because of higher marketing spending and slower bookings growth. Citigroup, however, listed Airbnb as one of the 33 large-cap stocks that are attractively valued after a pullback in stock prices over the first seven months of this year.

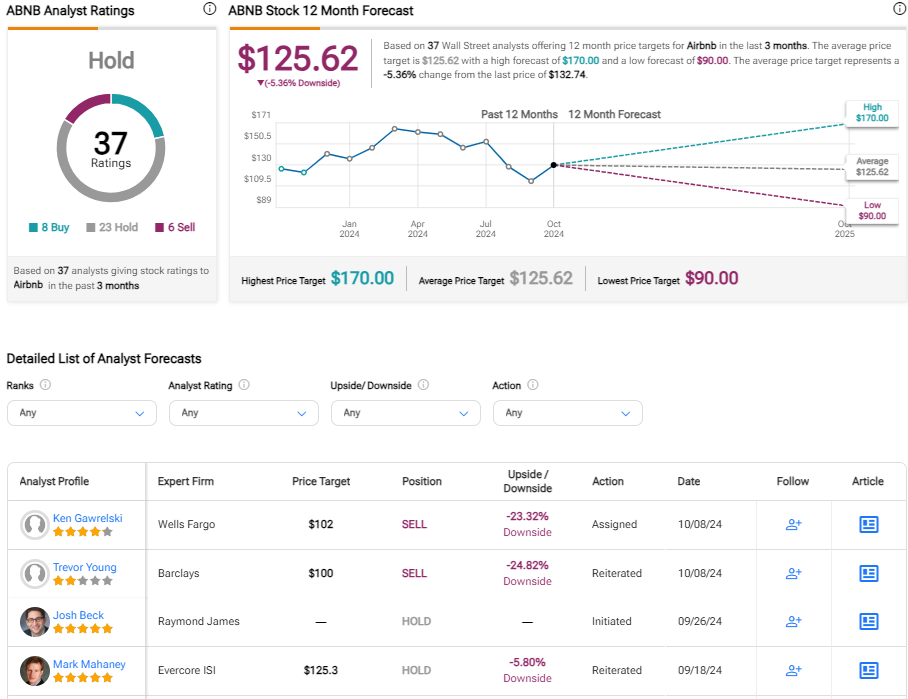

Based on the ratings of 37 Wall Street analysts, the average ABNB price target is $125.62, which implies downside of 4% from the current market price.

Despite pessimism on Wall Street, I am confident of Airbnb’s long-term growth potential at a time when the company is expanding into high-growth international markets while introducing new products to lure new customers. Airbnb is well-positioned to take market share from traditional travel booking platforms such as Booking Holdings by leveraging its relationships with hosts to offer unique, localized experiences. This market share growth is likely to lead to robust earnings growth and a meaningful expansion in valuation multiples.

Investment Takeaway

Airbnb has seen a deceleration in revenue and bookings growth in the last few quarters but Fed rate cuts are likely to keep travel demand elevated, paving the way for an acceleration in revenue growth. The company enjoys several long-term tailwinds amid changing travel industry dynamics and is capitalizing on these trends by continuing to expand into new markets and product categories. Long-term shareholders are likely to benefit from Airbnb’s continued market share wins.