Palantir Technologies (PLTR) has been a market favorite, soaring over 238% in the last year. While the data analytics giant continues to build incredibly strong business momentum, particularly across AI initiatives, several factors may warrant some caution at the current levels, which could pause PLTR’s upward climb. This makes me neutral in the short term. However, I am bullish on PLTR’s prospects for the long term, having carved a unique position in AI and data analytics.

Palantir Continues to Show Strong Execution

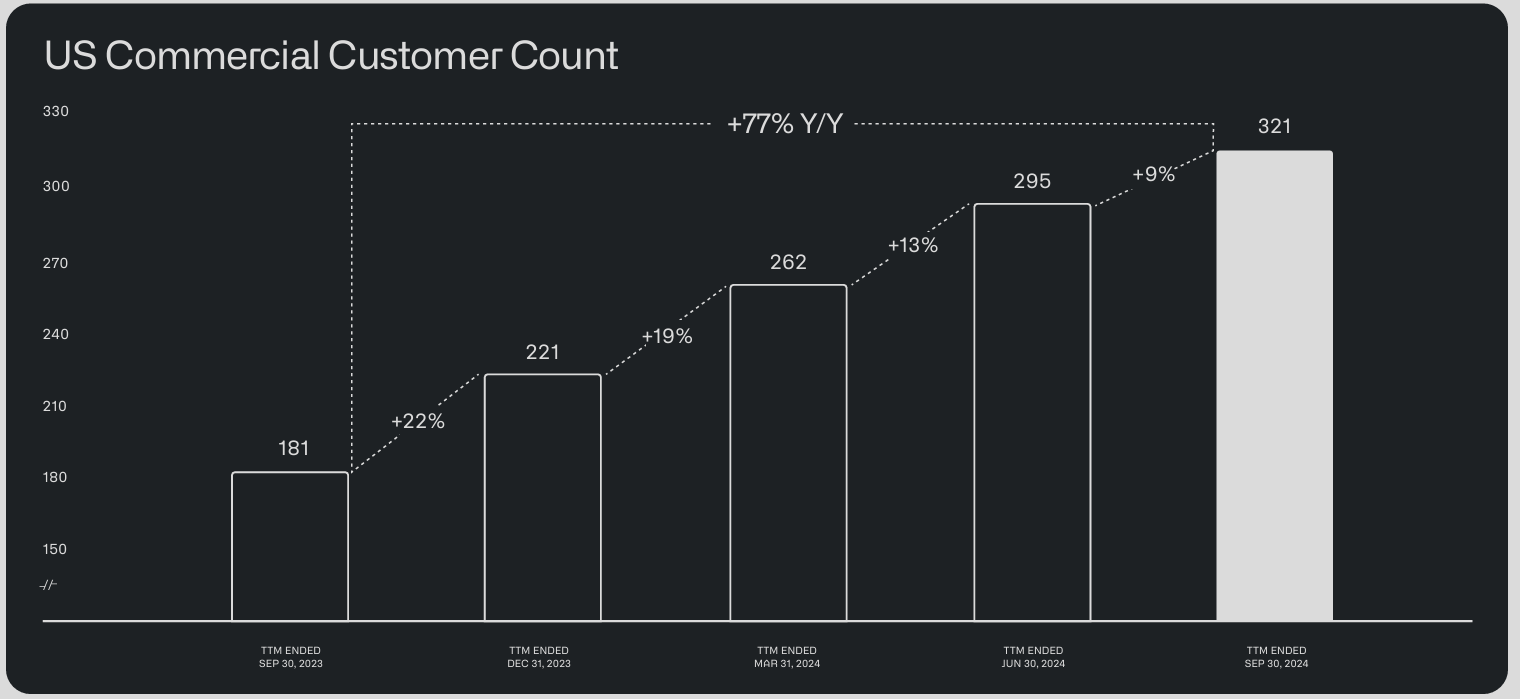

Despite my concerns, recent performance metrics show nothing but accelerating growth. In Q3 2024, management reported annual revenue growth of 30% to a whopping $725.5 million. U.S. commercial revenue grew by 54%, while U.S. government revenue increased by 40%.

Profitability is also moving rapidly in the right direction. In Q3, operating income was $113 million, and adjusted operating income reached $276 million. Notably, Palantir generated an adjusted free cash flow of $435 million in the quarter, representing an enormous 60% margin.

Building Reputation, and the Balance Sheet

I am also concerned about the share price, but Palantir’s Artificial Intelligence Platform (AIP) is undeniably a growth machine. With 104 deals over $1 million closed in the last quarter alone, the demand is huge, which only enhances my bullish sentiment for the long term.

Testimonials show that AIP is quickly making a real difference for customers. Building this reputation is gold dust in today’s environment, where almost every business fears being left behind by emerging AI technology. In addition, the firm’s finances remain incredibly robust, with a massive $4.56 billion in cash against $254.91 million in debt. This enables investments in product development and opens the door to strategic acquisitions as the sector advances.

Valuation Concerns Mount

Despite these fundamentals, I see a few red flags in the short term. At 43 times revenue, the share price eclipses industry peers. With a price-to-earnings (P/E) ratio of 325, investors appear to be pricing in extremely aggressive growth expectations, which may be challenging to meet.

Furthermore, market enthusiasm has pushed the market capitalization to $146.5 billion, which many will say seems disconnected from current financial metrics. While the company is executing well, this valuation leaves little room for operational hiccups. If the market takes a turn or if enthusiasm for AI-related companies declines, the share price could easily go down.

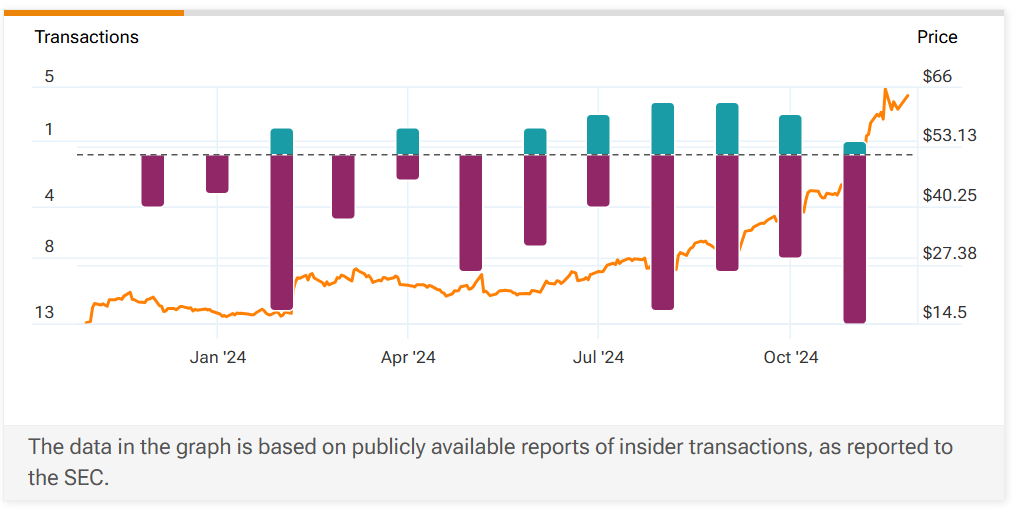

I’m also slightly concerned by insider sales patterns. Recent SEC filings show significant levels of insider selling, including a notable transaction from CEO Alex Karp, who sold shares worth over $200 million in the last week alone. While insider selling obviously doesn’t always indicate declining confidence in the company, I’d say the volume and timing of sales warrant some attention.

Mixed Signals from Wall Street

Wall Street analysts are also notably cautious on PLTR at current levels. Based on 16 analysts covering the stock, the consensus rating is Hold, with 3 Buys, 7 Holds, and 6 Sells. The average price target of $33.73 suggests a potential downside of 40.09% from current levels.

Recent price target revisions from Wedbush and Bank of America pushed targets to $75. Meanwhile, many firms, like Jefferies, warn of significant potential downside, highlighting the polarized views on the company’s future. I wouldn’t be surprised to see both sides of the argument have their moment at times, with volatility likely to feature in the sector for the foreseeable.

Competitive Positioning

Many analysts have expressed concerns about Palantir facing competition from established tech giants and emerging AI companies. Still, its deep expertise in handling sensitive government data seems to provide a significant moat. A track record of securing clearances and managing complex data environments creates barriers to entry that competitors will struggle to overcome.

However, the landscape is evolving. As more companies develop AI capabilities, Palantir must continue innovating to maintain a competitive edge. As I noted previously, maintaining technological leadership requires sustained and enormous R&D investments, and if the competition appears to be catching up, the market may get nervous.

Future Catalysts for Palantir

Despite my cautiousness in the near term, several catalysts could support a growth trajectory over the long term. Recent admission to the S&P 500 should drive increased institutional ownership of the stock and potentially provide more stability. Growing geopolitical tensions could also easily drive increased government spending on intelligence and defense technologies, benefiting the firm’s government segment.

Moreover, the expansion of AIP adoption presents another gigantic growth avenue, with the company securing a new five-year, $100 million contract to expand Maven Smart System AI/ML capabilities across U.S. military services. Developing new products like Visual Navigation (VNav) for autonomous drone missions shows promising innovation.

The Bottom Line

While Palantir’s technology leadership and execution are impressive, I believe the stock is significantly overextended. Most dangerously, the market appears to be pricing in years of flawless execution. Several red flags suggest a meaningful pullback could be imminent. The significant insider selling missed commercial revenue expectations, and nearly half of Wall Street analysts recommend selling or holding the stock at these levels, all pointing to near-term vulnerability.

But despite my near-term caution, I remain fundamentally bullish on Palantir’s long-term prospects. The company has carved out a unique position at the intersection of AI, big data, and national security – sectors that should see sustained growth over the coming decades.

For me, the key is to separate any short-term price action from long-term value creation. Palantir’s combination of government relationships, AI expertise, and improving financial metrics suggests the company will be significantly larger in five years. However, the path to that growth will likely include periods of price correction and consolidation. For long-term investors, these pullbacks should perhaps be viewed as opportunities to build positions in what remains one of technology’s most intriguing growth stories.