Last year proved to be a fairly bumper year for many companies operating in the technology space. With AI continuing to impress and excite, most products and services in the sector saw surging demand and blossoming share prices. Sadly, not all were invited to this party, with Adobe (ADBE) being one of the unlucky ones, which failed to keep up with the S&P 500’s 25% gain. With a 25% decline over the same period, many investors were concerned about management’s ability to capitalize on AI innovations, reflected in some disappointing guidance.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

However, as the company’s fundamentals continue to develop, I see potential for Adobe to impress over the coming years, therefore, I’m taking a bullish position on ADBE stock.

Adobe’s 2024 Performance

I suspect management will see 2024 as a fairly mixed year, but I’m rather bullish on the fundamentals emerging in the latest report. With 11% growth in annual revenues, now at $21.51 billion, there’s still plenty of demand for the company’s range of products. Operating cash flow also exceeded records at a very healthy $8 billion.

The balance sheet looks to be in a fairly solid place too, with healthy $7.5 billion cash reserves, and a declining debt situation.

As expected, the company’s Digital Media segment had a rather strong year, with flagship products such as Photoshop, Acrobat, and Illustrator pulling in $4.15 billion in revenue. Further diversification may be more sustainable with this area accounting for about 75% of overall revenues. Still, growth in other areas, such as Digital Experiences and specializing in enterprise marketing, reflects management’s understanding of the challenges.

Of course, every company is now exploring how AI can transform operations and the balance sheet. Adobe’s Firefly generative AI platform has now exceeded 16 billion generations, demonstrating impressive adoption among creative professionals and enterprises. Integrating this product into the suite of Adobe services could lead to significant performance improvements and also enhance the user experience.

Addressing Key Challenges

Despite my general bullishness, there were clearly enough reasons in 2024 for investors to shy away from this one. The majority will look to fairly weak guidance from the last report as the key reason. With many companies reporting enormous surges in growth, management’s 8% revenue growth guidance for 2025 hardly impressed. Of course, not all of the hype seen in other market areas is justified, but management must demonstrate a genuine market for products going forward as competition looks to build market share.

Established players in the sector, such as Microsoft (MSFT) and Salesforce (CRM), have equally compelling AI products and services that directly compete within Adobe’s core markets. With the ability to bundle products and add on AI services as a welcome bonus, Adobe may struggle to compete with the level of pricing power available to these giants. Furthermore, almost countless AI companies are moving rapidly to build products in new markets, making it an incredibly dynamic and unpredictable space for investors.

As a result, many analysts have suggested that management hasn’t quite nailed the approach to these new products. Where many AI products are behind a paywall, Adobe’s approach of bringing users to the table and trying to monetize may be out of kilter with the competition, missing out on valuable revenues.

Adobe on a Steady Path to Recovery

Despite this challenging environment, I think the company is on the right track. By building a single suite across a range of impressive products, AI systems can enhance outputs across Creative Cloud, Document Cloud, and Experience Cloud without leaving the workflow. Where an external AI system was used, this experience can be clunky and ineffective, so I see real benefits to the whole process being built in a single system. Management reports that such efforts in Acrobat, such as intelligent document editing, make these tasks four times faster on average.

Such AI-assisted tasks aren’t exactly ground-breaking these days, but I think the new developments in Firefly around advanced video modeling could be another level up. Such a move could immediately create enormous monetization opportunities. The adoption of this higher-priced system by companies like Pepsi and Alphabet shows that at present, few systems can compete, giving first-movers an advantage in a critical area of the AI story.

As I noted, Adobe’s business experience will potentially be a huge benefactor of this progression. With $1 billion in bookings in 2024, including from BMW (BMW), Disney (DIS), and Procter & Gamble (PG), there could be enormous demand in the coming years for enhanced marketing and customer experiences driven by high-quality video generation. The launch of GenStudio will compound this, providing an end-to-end solutions provider for enterprises of all levels navigating this digital transformation.

Assessing Analyst Sentiment

I see many reasons to be bullish here, but analysts seem cautiously optimistic. Many align with my thesis that a recurring revenue base and some impressive AI tools could lead to further growth, but plenty point to slower-than-expected growth and a lack of clarity around monetization opportunities as major risks.

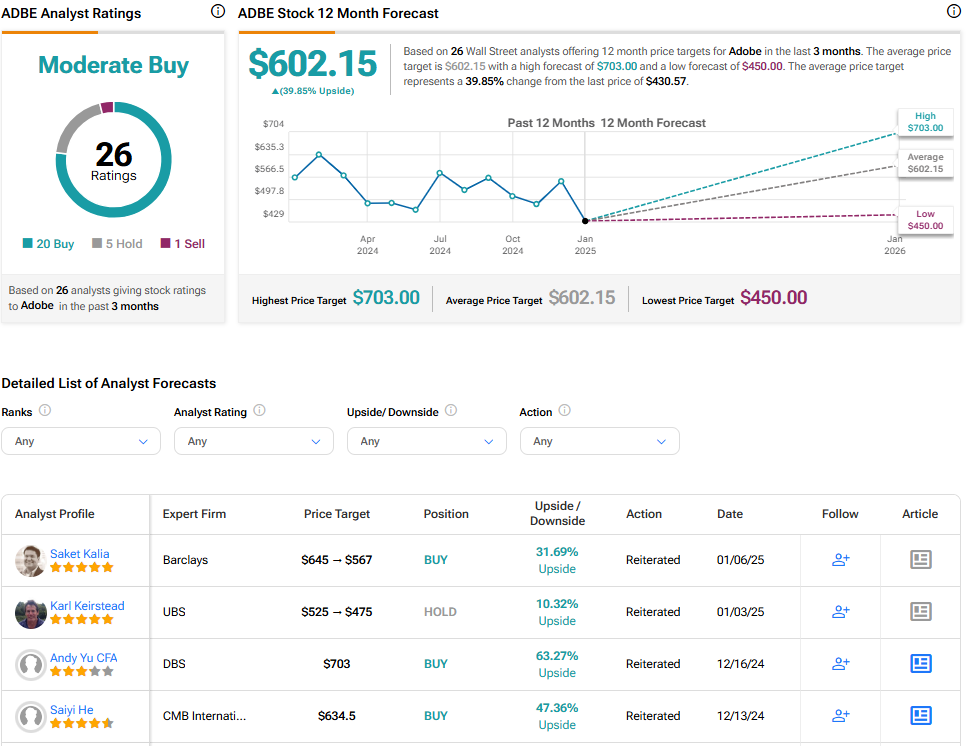

From my perspective, there is plenty of margin for safety here, with analysts placing an average price target of $604, a full 40% higher than the current level.

I’m also encouraged to see continued buybacks from management, reflecting a share price potentially below intrinsic value. Of course, this could be deployed in areas more aligned with the growth story seen in other companies, but I always see it as an encouraging sign when management looks to strengthen the balance sheet at the same time.

Summing Up

From my perspective, 2024 was a year of two stories for the company. The share price was disappointing, falling behind many competitors and the wider market, but the fundamentals and products were generally impressive. Lower guidance is hard to escape when it comes to market performance, but I can see why management would look to be cautious amid a turbulent time.

Looking ahead, I see Adobe on a path to recovery that hinges on monetizing its products over the coming years and building a genuinely useful AI-driven suite of products across a range of areas. So, while the road to recovery may not be smooth, I’m bullish on this one’s potential for years to come.