Speculation on the growth of electric vehicles is not exactly a new concept for investors, but the surrounding supply chain and emerging technology seem to be evolving by the day. One of the areas with the most potential is the materials required for the batteries in electric vehicles, lithium, in particular. Although relatively ubiquitous, mining and refining the raw material is big business, and mining giant Rio Tinto (RIO) looks to be the latest entrant to the sector, with a whopping $2.5 billion investment. As a result, I’m bullish on the company and see a big future for this revenue stream if demand grows as expected over the long term.

Rio Tinto’s Investment in the Rincon Project

Although the company has an established reputation in mining various precious metals, the recent foray into lithium is a relatively new area. By developing a 3,000-ton starter plant with plans to grow it by a further 57,000 tons in time, Rio Tinto looks set to own one of the largest lithium reserves in the world. By yielding over 60,000 tons annually from the so-called “Lithium Triangle” of Argentina, the firm will have enormous influence in the sector’s future, with the ability to build potentially lucrative partnerships with electric vehicle and battery manufacturers globally.

Lithium mining is a fairly established sector, too, of course, but the technology in use at the Rincon project looks set to use direct lithium extraction (DLE), a much less wasteful method than others, most notably for water. This positions the firm as a responsible operator in a sector often criticized for environmental damage.

I’m also encouraged that the reserves have been revised upwards by over 60% since the acquisition, suggesting that operations will support well over 40 years of operation. With the first production expected by 2028, I think this is an effective timeline to develop the right systems and structures, just as demand for EV batteries escalates.

Demand Is Growing Across Sectors

Although this level of demand can fluctuate across geographies and amid economic or geopolitical developments, the long-term trend for EV demand is clearly increasing. In 2023, just 14% of global car sales were electric, compared to more than 50% projected by 2030. While EVs will undoubtedly form a large portion of future lithium demand, energy storage systems are expected to be a critical element of the global transmission grid, with renewable generation often too inconsistent for the grid.

As customers and governments look to more resilient energy grids and sustainable energy solutions, I see lithium miners seeing major growth over the coming decades. Lithium prices have indeed been rather volatile as the market works through these forecasts. With global averages now generally back at the levels seen before market hype drove them to record highs, I sense there is now an opportunity for investment to return to the sector.

Strategic Growth for Rio Tinto

The investment in Rincon is naturally a risk, but I feel like it’s necessary in today’s landscape. While the company has typically specialized in mining iron ore, aluminum, and copper, diversifying across a wider range of sectors feels essential to me, as the mining sector’s cyclicality and volatility have challenged investors for some time. The Rincon investment will tap into the growing technology and energy sectors while traditionally providing stability to the mining sector.

I also see a unique opportunity for the company, with Argentina’s political regime moving to a pro-investment policy that includes multiple tax breaks, regulatory stability, and encouraging partnerships.

The wider company is performing well despite challenging market conditions. I’m also encouraged to see the P/E ratio of just 9.4 reflecting some major potential in the share price as the market digests the new investment. From a basic discounted cash flow (DCF) calculation, I’d see another 25% upside, taking the shares to just under $80.

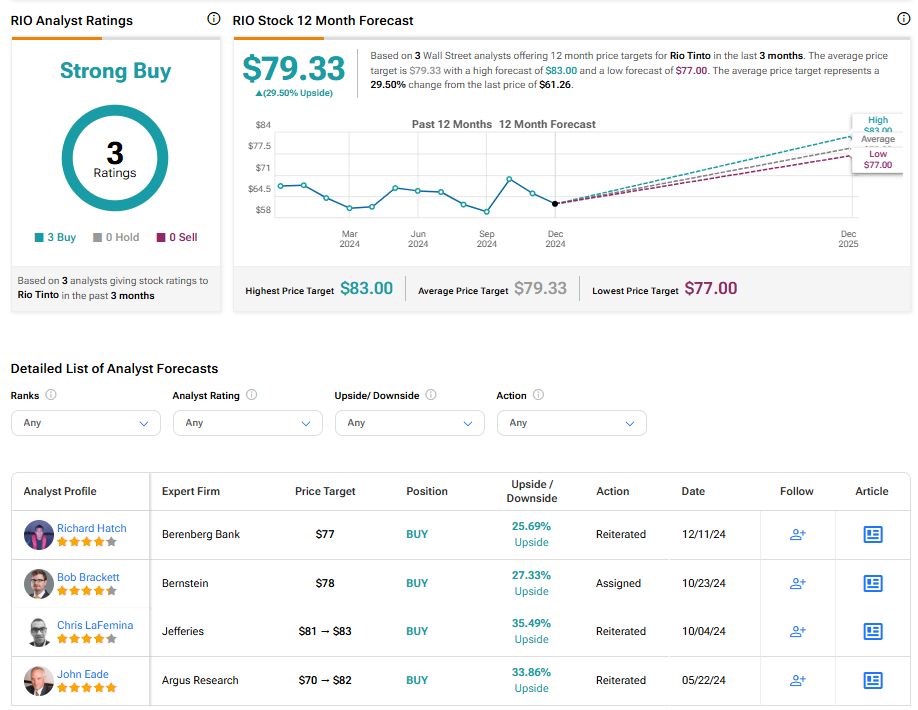

Wall Street Sees Potential Too

Many Wall Street analysts share my optimism. They have an average price target of $79.33, an impressive 29.50% higher than the current price.

With a generous 6.96% dividend yield, too, many investors will see the growth potential as just another reason to like the company. At a payout ratio of 56%, there’s a decent amount of room for management to boost this if required, bringing further stability to investors looking for opportunities.

Challenges Emerging for Rio Tinto

Despite my bullishness, the sector clearly has several challenges to overcome in the next few years. As I noted, the political system in Argentina is currently very favorable to the project, but this could easily change. Such a pivot could be a major red flag for investors, pushing the share price down even further after a disappointing few years.

The company is also relatively new to the lithium business. By using DLE technology, which is somewhat unproven at such a scale, the project could easily see downward revisions in output if operations are not as efficient as currently thought.

The volatility of global lithium prices also reflects an ongoing risk, but my expectation is that this trends higher over the coming decades, and would be well diversified when considering the wider mining portfolio of the company.

Summing Up

Overall, I’m encouraged to see the company moving into the lithium market, with strong potential for long-term demand in high-margin markets. The company’s proven track record in large-scale projects and experienced management make it a compelling investment, especially when considering the dividend yield and current valuation. While a $2.5 billion investment is clearly a big risk, I see it as one that could define the company’s future for decades to come.