Affirm Holdings, Inc. (AFRM) has reported a loss in the fiscal first quarter of 2022 but revenues beat analysts’ expectations. Additionally, the company has provided upbeat revenue guidance and announced the expansion of its relationship (entered in August) with Amazon (AMZN).

Invest with Confidence:

- Follow TipRanks' Top Wall Street Analysts and uncover their success rate and average return.

- Join thousands of data-driven investors – Build your Smart Portfolio for personalized insights.

Following the news, shares of the digital and mobile-first commerce platform jumped 27.3% in the extended trading session on Wednesday after closing 15.4% lower on the day.

Results in Detail

Affirm incurred a loss of $1.13 per share, higher than a loss of $0.06 per share in the same quarter last year.

Total revenues generated during the quarter stood at $269.4 million against the consensus estimate of $248.23 million. Revenues grew 55% year-over-year on the back of network revenue, which was driven by gross merchandise volume (GMV) growth and interest income. (See Affirm stock charts on TipRanks)

Total network revenue came in at $111.6 million, up 12.5% year-over-year. Additionally, interest income more than doubled to $117.3 million.

For the reported quarter, GMV stood at $2.7 billion, up 84% year-over-year. While active merchants increased from 6,500 in the same quarter last year to 102,000, active consumers grew 124% to 8.7 million.

Other Developments

With its expanded relationship with Amazon, Affirm will support all purchases of $50 or more on Amazon.com and the Amazon shopping app in the United States. As part of the revised agreement, the company will act like Amazon’s only third party, non credit card, buy now, pay later (BNPL) option in the U.S. Additionally, Affirm will be integrated into Amazon Pay’s digital wallet in the U.S.

CFO Comments

The CFO of Affirm, Michael Linford, said, “During the first quarter, we continued to scale our two-sided network, delivering robust top-line growth, strong unit economics and even greater capital efficiency. We are seeing traction across all products and verticals, and deepening our trusted relationships with merchants and consumers alike. As we continue to capitalize on our hyper growth phase, we are strongly positioning ourselves for the long-term by investing in our key competitive advantages in technology and talent.”

See Insiders’ Hot Stocks on TipRanks >>

Outlook

For the second quarter of Fiscal 2022, the company projects revenue to be in the range of $320 million to $330 million versus the consensus estimate of $296.06 million. GMV is expected to land between $3.55 billion and $3.65 billion versus the Street’s estimate of $3.27 billion.

For Fiscal 2022, the company projects revenues to be in the range of $1.225 billion to $1.250 billion, up from the previous guidance of $1.16 billion to $1.19 billion. Analysts’ expectations are pegged at $1.2 billion. GMV is expected to land between $13.13 billion and $13.38 billion.

Wall Street’s Take

In response to strong quarterly results, Mizuho Securities analyst Dan Dolev reiterated a Buy rating and a price target of $170 on the stock.

The rest of the Street is cautiously optimistic about the stock and has a Moderate Buy consensus rating based on 7 Buys, 4 Holds and 1 Sell. The average Affirm price target of $148.64 implies 11.32% upside potential. Shares have gained 37.32% over the past year.

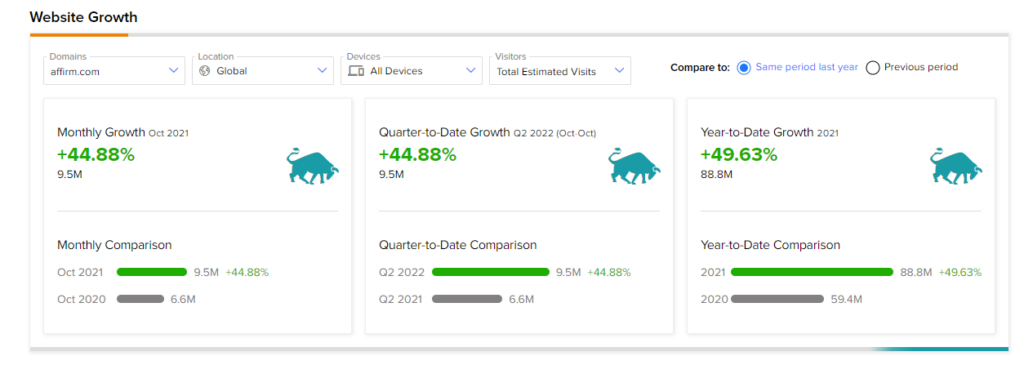

Website Traffic

TipRanks’ Website Traffic Tool, which uses data from SEMrush Holdings (SEMR), the world’s biggest website usage monitoring service, offers insight into Affirm’s performance. According to the tool, the Affirm website recorded a 44.88% monthly growth, year-over-year, in global visits in October.

Similarly, year-to-date website growth, compared to year-to-date website growth in the previous year, came in at 49.63%.

Related News:

Amazon Expands in Alabama with New Operational Sites

Pfizer & Biohaven Join Hands for Commercialization of Rimegepant

Upstart Provides Upbeat Q4 Outlook on Better-than-Expected Q3 results