Advance Auto Parts (AAP) is facing severe financial headwinds. Poor inventory management, declining margins, and high debt levels have impacted the bottom line and drove the stock down almost 23% over the past year. While the recent $1.2 billion sale of Worldpac has freed up much-needed cash, it has also underscored deeper financial issues at the heart of the business, leading to a projected further EBITDA reduction of $130 million.

Despite revenue stabilization, margins continue to dwindle due to rising costs and investments in pricing, which negatively impact profitability and cash flow. As a result, AAP’s turnaround appears to be long-term engagement, with high-value trap potential for investors.

Advance Auto Parts Sells Subsidiary to Focus on Core Business

Advance Auto Parts operates a significant network of 4,776 stores that provide automotive aftermarket parts in the United States, Canada, Puerto Rico, and the U.S. Virgin Islands. Its distribution extends to 1,138 owned Carquest branded stores in Mexico and various Caribbean islands. AAP’s extensive product portfolio offers automotive replacement parts, accessories, batteries, maintenance items, and numerous automotive-specific products for various vehicle types.

Recently, Advance Auto Parts announced a definitive agreement to sell its prominent wholesale distribution business, Worldpac, Inc., to funds managed by global investment firm Carlyle (CG) for $1.5 billion in cash (net proceeds of about $1.2 billion). The sale is expected to close by year-end, and the firm plans to use these proceeds primarily to bolster its balance sheet and invest in the business.

Advance Auto Parts Recent Financial Results & Outlook

The company recently reported its second-quarter results for 2024. Revenue of $2.68 billion was flat year-over-year but slightly surpassed analysts’ estimates of $2.67 billion. The company saw a minor increase of 0.4% in comparable store sales. However, the gross profit margin decreased from 42.5% to 41.5%, resulting in a gross profit of $1.1 billion. The decrease was attributed to strategic pricing investments and increased product costs. Operating income was reported at $71.8 million, or 2.7% of net sales, compared to 4.7% in Q2 of 2023. Earnings per share (EPS) of $0.75 fell below analysts’ estimates of $0.92.

The company also improved its cash flow, with net cash provided by operating activities of $87.8 million compared to $167.1 million in Q2 2023. Further, the company announced a cash dividend of $0.25 per share to be paid in October to all common stockholders.

AAP’s management has offered guidance for 2024, projecting net sales between $11.15 billion and $11.25 billion. Comparable store sales are expected to fluctuate between a 1.0% decrease and no change. Operating income margin is forecasted to range between 2.1% and 2.5%. The diluted EPS is projected to be between $2.00 and $2.50.

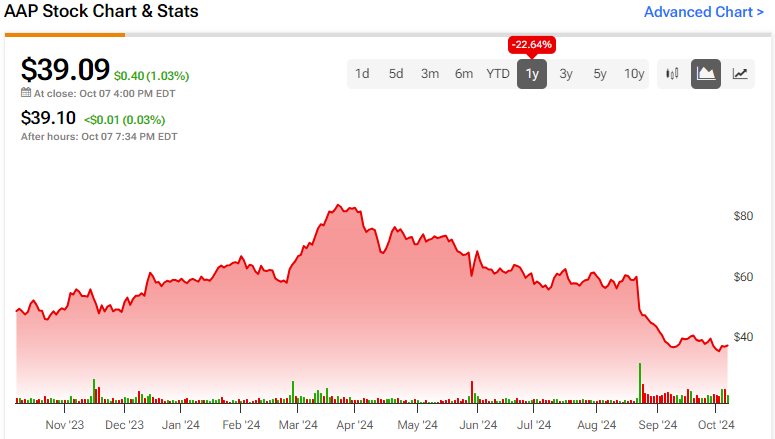

What Is the Price Target for AAP Stock?

The stock has been on an extended downtrend, shedding over 80% in the past three years. It trades at the low end of its 52-week price range of $36.40 – $88.56 while showing ongoing negative price momentum by trading below its 20-day (41.01) and 50-day (47.22) moving averages. The stock trades at a significant discount to industry peers, with a P/S ratio of 0.2x, compared to the Specialty Retail industry average of 1.0x.

Analysts following the company have taken a cautious stance on AAP stock. Based on 14 analysts’ cumulative recommendations, Advance Auto Parts is rated a Hold. The average price target for AAP stock is $54.46, representing a potential upside of 39.32% from current levels.

Final Analysis of AAP

Advance Auto Parts has responded to financial challenges by focusing on strategic maneuvers to improve its fiscal standing, including the recent sale of Worldpac. While this has provided a cash injection, it hasn’t fixed the deeper financial issues, such as rising costs and pricing investments impinging on margins. Management has its hands full trying to engineer a long-term turnaround. The stock trades at a significant discount compared to industry peers.

However, the combination of business challenges suggests that AAP may pose more of a value trap than a value trade. Investors may want to wait for tangible signs of improvement before entertaining the stock.