Adobe (ADBE), the leader in creative software, is set to report its third-quarter earnings on September 12 and I maintain my Buy stance on the stock heading into the event. My optimism is backed by the positive sentiment on Wall Street and the company’s strong fundamentals. Analysts have revised Q3 expectations upwards following Adobe’s encouraging guidance in Q2, reigniting bullish sentiment toward the stock. Moreover, Adobe’s stock price sitting above multiple key moving averages provides further confirmation of a strong bullish trend.

Additionally, Adobe’s valuation is currently lower than at the start of 2024 and is at the lower end of its historical range. Despite the challenges of pricing in generative artificial intelligence’s (AI) impact, Adobe’s upward revision of its Fiscal 2024 guidance and the company’s strong fundamentals support long-term optimism for the stock. The Q3 results will be a key factor in this outlook.

The Case for Liking Adobe

My optimistic stance on Adobe is grounded in the high quality of its business fundamentals, including its industry-leading position and growing potential in AI. Here are the main points in detail:

- Dominant Market Position: Adobe is a leader in graphic processing software with approximately 80% market share and holds around 20% of the global document processing software market. This dominant position in its Creative and Document Cloud services segments gives it a significant competitive advantage over its peers.

- Strong Financials: Adobe operates with a subscription-based business model, with subscriptions accounting for over 90% of its revenue. The company boasts a high free cash flow margin of about 32% (compared to an industry average of 10.5%) and has achieved rapid revenue growth, with a 15% CAGR (compound annual growth rate) over the past five years. This growth is impressive for a mature, market-leading company.

- Growth Potential in AI: Adobe is well-positioned to capitalize on the opportunities presented by generative AI, leveraging its extensive use cases in creativity. Its suite of creative tools, including Photoshop, Illustrator, and Premiere Pro, can be significantly enhanced with AI. This positions Adobe to expand its product offerings, capture new markets, and drive long-term growth potential, ultimately enhancing customer satisfaction and retention.

Where Adobe Stands Today

The bullish thesis on Adobe has been further reinforced by the recent turnaround in its stock performance, which may reflect the positive advances in its business fundamentals. Although Adobe stock has been relatively flat throughout this year, there has been noticeable bullish momentum since the Q2 results in June.

Three months ago, Adobe reported strong quarterly results, surpassing both top and bottom-line expectations. The company achieved about a 15% year-over-year increase in its adjusted EPS and a 10% rise in revenue. It also registered a robust $1.94 billion in cash flow from operations and repurchased 4.6 million shares during the quarter.

What stood out most was Adobe’s updated guidance. The company raised its revenue forecast range for Fiscal 2024 to $21.40 billion to $21.50 billion from the previous guidance of $21.30 billion to $21.50 billion. ADBE also increased its adjusted EPS forecast to the range of $18.00 to $18.20 from the prior outlook of $17.60 to $18.00. This positive update led to a rally in Adobe shares, which rebounded from their mid-year lows.

Currently, Adobe trades at a forward price-to-earnings (P/E) ratio of 31x. This is lower than at the beginning of 2024 and is on the lower end of its historical valuation range. For context, Adobe’s forward P/E ratio exceeded 48x in July 2021 but fell to around 13x at its lowest point. Although the valuation has increased from those lows in 2022 and 2023, it is still not up on the year. In fact, Adobe is trailing major indexes, and the recent bounce represents just a slight recovery from the stock’s previous lows of around $430 per share after starting the year close to $600.

What to Expect from Adobe in Q3

My optimism ahead of Adobe’s earnings mirrors the general sentiment on Wall Street as we approach the Q2 earnings event.

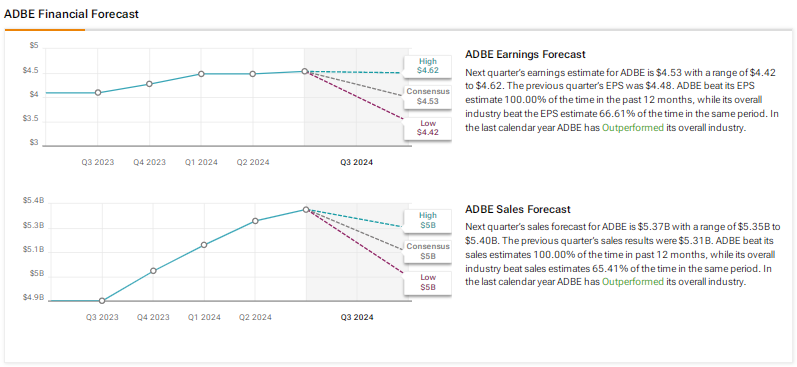

For its upcoming earnings report, market expectations are positive. Adobe is expected to report EPS of $4.53 and revenue of $5.37 billion, which would represent annual increases of about 11% and 10%, respectively. In the past three months, 28 analysts have revised their EPS projections upwards, while 20 analysts have raised their revenue forecasts.

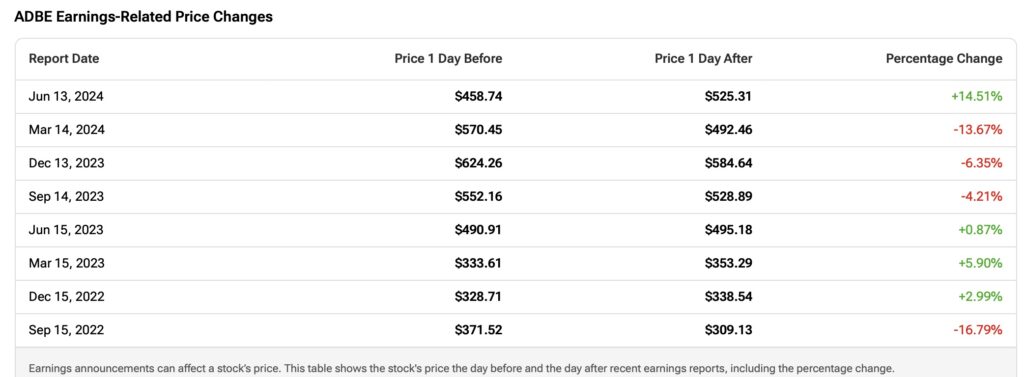

Adobe’s track record is favorable, as the company has consistently exceeded bottom-line estimates in each quarter since at least August 2019. However, this does not necessarily guarantee a positive reaction after earnings reports. Adobe stock has shown negative price changes following earnings in three of the past four quarters.

Risks to Watch for in Adobe Stock

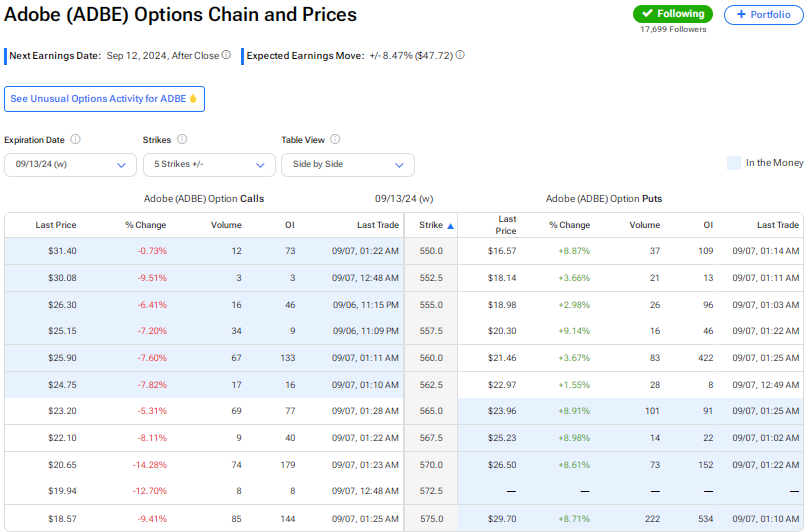

The main caution for Adobe’s positive momentum is that Q3 is expected to witness continued volatility, as indicated by the options chain. The expected price movement, based on the at-the-money straddle expiring on September 13, is 8.47%.

Therefore, even if Adobe beats earnings estimates, this may not ensure a positive reaction. Data suggesting a slowdown in AI investment or weaker-than-expected gains from AI efficiency could lead to a more negative market response.

Furthermore, Citigroup (C) analyst Tyler Radke has highlighted an increase in Creative Cloud’s promotional activity, indicating a potentially more price-sensitive and competitive market than in previous years. This trend could constrain Adobe’s ability to raise prices without impacting subscription growth, particularly among individual users.

Is ADBE Stock a Buy, According to Analysts?

The Wall Street consensus on Adobe is predominantly bullish, with a Moderate Buy rating. Of the 28 analysts covering the stock, 21 have a Buy recommendation, five have a Hold rating, and only two have a Sell recommendation. Despite this overall optimism, the upside potential is somewhat limited. The average ADBE stock price target is $613.85, suggesting an upside potential of 8.95% from the current share price.

Key Takeaways

Adobe’s Q3 earnings report is expected to reinforce the bullish outlook, driven by recent positive revisions in both revenue and earnings expectations. With strong guidance and a solid track record, I am confident that the integration of AI into Adobe’s innovative product roadmap will highlight the company’s continued growth and potential for stock appreciation. This is especially true given that the stock’s current valuation is lower than it was earlier in 2024.