Abercrombie & Fitch (ANF) shares have dropped over 20% in the past few days, partly due to lower-than-expected Q1 and fiscal 2025 guidance. Even though Wall Street analysts were projecting more robust sales growth, the apparel retailer predicts only a 3-5% increase over the year. Earnings per share are also projected to fall short of expectations in the next quarter, ranging between $1.25 and $1.45 instead of the anticipated $1.97. While the company experienced solid growth in the past two years, the latest outlook indicates a slower pace partially attributed to the potential impact of tariffs on freight costs and consumer spending. Despite the downturn, Abercrombie & Fitch continues to focus on maintaining its customer value perception without introducing significant changes in pricing.

Bracing for Tariff Impacts

Abercrombie & Fitch is a specialty retailer that provides clothing and accessories for various age groups, from children to millennials. It manages a variety of brands, such as Abercrombie and Hollister, and operates around 790 brick-and-mortar stores across North America, Europe, Asia, and the Middle East.

Joining a list of other U.S. retailers facing a potentially challenging year, ANF has warned about weak annual sales growth and a possible softened demand for its brand this spring. The company highlighted a $5 million impact from U.S. tariffs and mentioned that margins would be negatively affected due to higher freight costs and increased promotions designed to clear excess inventory.

Further, normalized carryover inventory selling is expected to negatively affect the first half of the year. The second half, however, might see some reprieve with lower freight costs than the previous year. CFO Robert Ball has indicated that potential price hikes, although slight, might be on the horizon as the company strives to maintain a favorable value perception among customers.

Top and Bottom-Line Beats Amid Soft Guidance

For the fiscal fourth quarter that ended on February 1, 2025, the company reported net sales increased by 9% year-over-year, reaching $1.58 billion; operating income reached $256 million, an increase from last year’s $223 million; operating margin increased to 16.2% from the previous year’s 15.3%; and a net income per diluted share of $3.57 beat analyst expectations.

For the fiscal year 2025, the company anticipates net sales to grow from 4% to 6% in the first quarter and 3% to 5% for the entire year. The operating margin is expected to range from 8% to 9% for the first quarter and 14% to 15% for the year. Estimated net income per diluted share ranges from $1.25 to $1.45 for the first quarter and from $10.40 to $11.40 for the entire year. The company also plans on repurchasing shares worth $100 million in the first quarter and $400 million for the entire year.

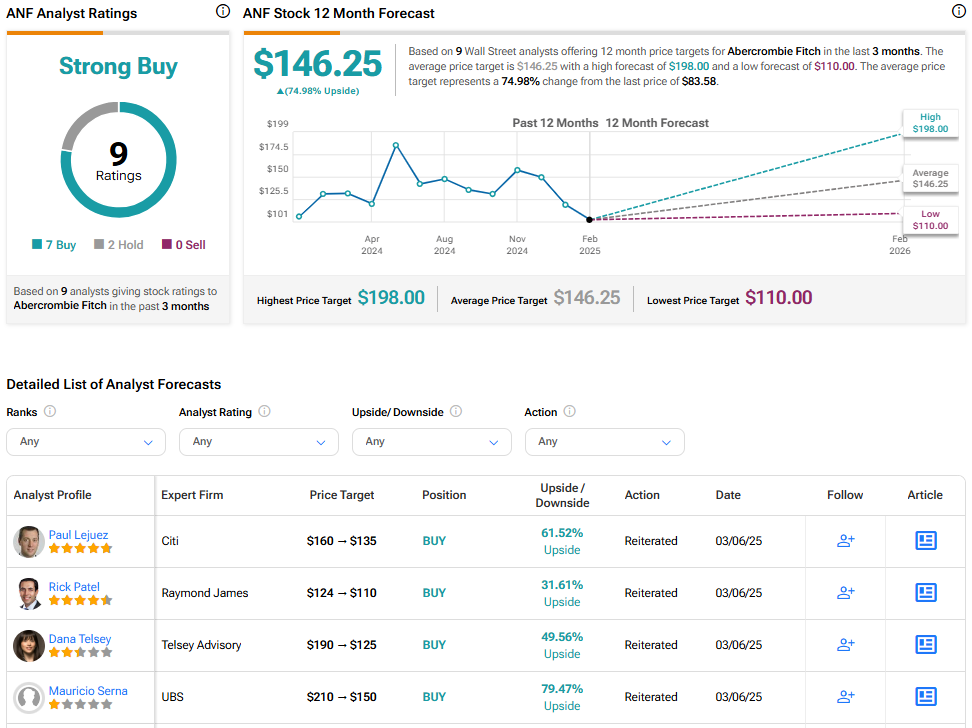

Analysts Lower Price Targets

Analysts following the company remain bullish on its long-term prospects, though many have lowered their 12-month price targets after the recently soft forward guidance.

For example, Telsey Advisory, Raymond James, and UBS have all lowered their price targets for Abercrombie & Fitch despite maintaining positive ratings on the shares. Telsey Advisory dropped its target from $190 to $125, pointing to strong year-end results. Meanwhile, Raymond James reduced its target from $124 to $110 due to factors such as freight-induced gross margin contraction but indicated the fiscal 2025 revenue forecast was achievable, taking into account the new CFO and the strength of Hollister and control of SG&A. UBS adjusted its price target from $210 to $150, highlighting that Abercrombie & Fitch’s brands continue to outperform competitors in the specialty retail space and retain solid fundamentals. They projected a 10% five-year compound annual growth rate for EPS, which they believe is undervalued.

Abercrombie Fitch is rated a Strong Buy overall, based on the recent recommendations of nine analysts. The average price target for ANF stock is $146.25, which represents a potential upside of 74.98% from current levels.