Schrodinger (SDGR) provides software solutions to the pharmaceutical industry. It also engages in drug discovery and has several drug candidates for which it plans to begin seeking FDA marketing approval.

Let’s take a look at Schrodinger’s latest financial performance, drug development programs, and risk factors.

Schrodinger’s Q2 Financial Results and Full-Year 2021 Guidance

The company reported a 29% year-over-year increase in revenue to $29.8 million for the second quarter, in line with consensus estimates of $29.88 million. The software business is Schrodinger’s main revenue source. In Q2, software revenue increased 15% year-over-year to $24.1 million. Drug Discovery revenue rose to $5.7 million from $2.2 million in the same quarter last year.

Schrodinger posted a loss per share of $0.49, which widened from a loss per share of $0.05 a year ago, and missed consensus estimates of a loss per share of $0.33. (See Schrodinger stock charts on TipRanks).

For full-year 2021, the company anticipates revenue in the range of $124 million – $142 million. Consensus estimates call for revenue of $138.8 million. The company expects software revenue of $102 million – $110 million.

Schrodinger’s Drug Discovery Programs

In August 2021, Schrodinger announced a partnership with Zai Lab (ZLAB) to develop an oncology program. Schrodinger will receive a 50% share of the profits from U.S. sales. Further, Schrodinger will receive royalties on sales outside the U.S. Schrodinger will also be eligible for milestone payments of up to $338 million.

Schrodinger also has a separate drug discovery partnership with Ajax Therapeutics. It said that Ajax recently raised $40 million to support its drug development program.

Schrodinger plans to seek FDA approval for three of its internal drug candidates in 2022. The company is also continuing research to expand its internal product pipeline.

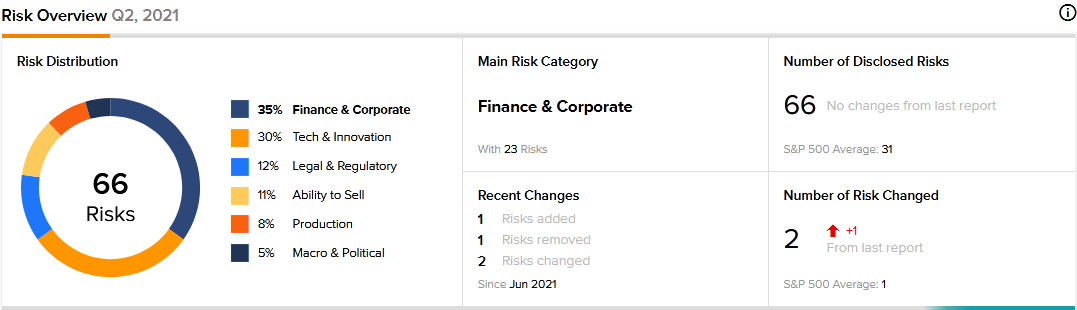

Schrodinger’s Risk Factors

The new TipRanks Risk Factors tool reveals 66 risk factors for Schrodinger. Since December 2020, the company has updated its risk profile to add one new risk factor under the Finance and Corporate category.

The company tells investors that it has been enjoying the benefits of an emerging growth company (EGC), as defined in the JOBS Act. For example, it has been exempt from certain disclosure requirements that generally apply to public companies. But Schrodinger is due to lose its EGC status on December 31. The company cautions that the loss of EGC status will cause its financial and legal compliance costs to rise significantly. Further, failure to meet the additional compliance requirements could cause its stock price to decline.

Finance and Corporate is Schrodinger’s top risk category, accounting for 35% of the total risks. That is below the sector average at 39%. Schrodinger’s shares have declined about 26% since the beginning of 2021.

Analysts’ Take

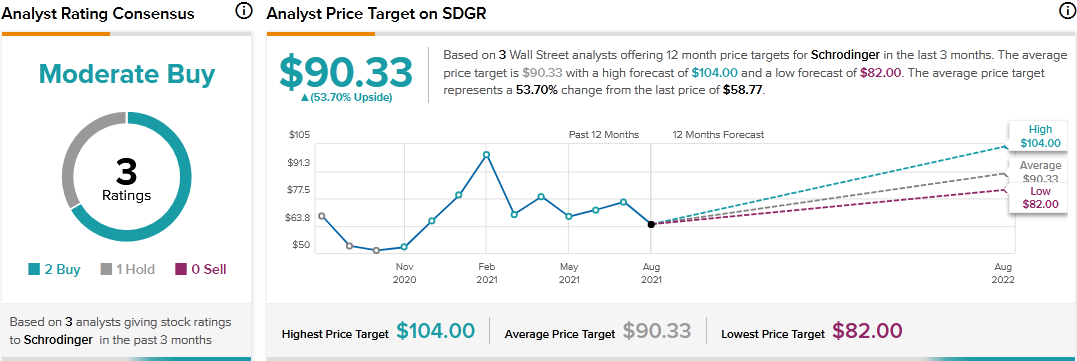

Morgan Stanley analyst David Lebovitz recently reiterated a Hold rating on Schrodinger stock but lowered the price target to $82 from $83. Lebovitz’s reduced price target still suggests 39.53% upside potential.

Consensus among analysts is a Moderate Buy based on 2 Buys and 1 Hold. The average Schrodinger price target of $90.33 implies 53.70% upside potential to current levels.

Related News:

A Look at GrowGeneration’s Earnings and Risk Factors

Medtronic Q1 Results Beat Estimates; Shares Pop 3%

What Does GCM Grosvenor’s Newly Added Risk Factor Tell Investors?