Twilio (TWLO) stock’s market-beating rally from early 2024 ended after it published its Q4 earnings on February 13. Despite TWLO’s solid financial performance and prudent strategic initiatives, the market gave the stock a beating. However, the cloud communications platform has a few aces up its sleeve and has been discounted too soon. With the shares down 20% since the earnings call, investors may be looking at TWLO’s depressed price for an enticing entry point.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

I’m bullish on the software company, noting improving performance across key metrics and an improved valuation proposition. Moreover, its use of artificial intelligence (AI) appears to streamline operations and enhance its product offering.

Twilio’s Earnings Selloff Overreaction

Twilio’s Q4 2024 results demonstrated underlying resilience despite mixed headlines, with several key metrics signaling operational progress. Revenue grew 11% year-over-year to $1.19 billion – accelerating from 4.5% growth two quarters earlier – and surpassed estimates by $13 million. The Communications segment drove this performance with 12% growth, buoyed by record Cyber Week messaging volumes (5 billion messages) and expanded enterprise contracts, including a major U.S. healthcare system adopting RCS and branded calling.

Meanwhile, operational discipline delivered Twilio’s first-ever GAAP operating profit ($14 million), while non-GAAP operating income rose 14% to $197 million. Deferred revenue and customer deposits reached new highs, and the dollar-based net expansion rate improved to 106%, its strongest since Q1 2023.

Though a $17 million bad debt provision tied to a Brazilian customer temporarily dented margins, cost controls expanded non-GAAP operating margins to 16.5%. Management’s conservative 2025 guidance (7-8% revenue growth) reflects caution, but $3 billion projected cumulative free cash flow through 2027 and a healthy balance sheet ($2.3 billion net cash) underscore long-term flexibility.

All considered, I believe the 20% selloff is overdone. However, this is often the way with surging stocks. Investors hoped for a more significant beat to sustain the share price momentum.

Twilio Can Be an AI Winner

Twilio strategically embeds artificial intelligence (AI) across its platform to enhance customer engagement and operational efficiency. Its partnership with OpenAI integrates real-time API capabilities for building conversational AI apps, enabling dynamic voice interactions through solutions like Conversation Relay.

The company’s Studio 2.0 platform now employs AI-driven routing to personalize customer journeys, leveraging CRM data for context-aware decisions between human agents and AI assistants. Compliance Toolkit—currently in beta—uses AI to automate regulatory adherence by scanning opt-out databases, verifying phone numbers via FCC records, and blocking non-compliant messages.

Twilio’s Valuation isn’t an Issue

Twilio’s valuation presents an intriguing picture and potentially enticing. Firstly, the company’s market capitalization is $19.2 billion, with an enterprise value of $17.9 billion, reflecting a strong net cash position. Meanwhile, the stock is trading at 29x forward earnings, representing a 13% premium to the information technology sector.

However, as always, we need to consider growth. The average earnings growth rate over the medium term is 23.5%, leading us to a forward price-to-earnings-to-growth ratio of 1.23. Notably, this is significantly lower than the information technology sector average of 1.84, suggesting that Twilio may be undervalued relative to its growth prospects.

This attractive PEG ratio aligns well with Twilio’s improving financial performance. The company recently reported its first-ever quarter of GAAP operating profitability and has demonstrated consistent revenue growth.

Additionally, Twilio boasts a strong track record of beating earnings and revenue estimates, with only one earnings miss in the past five years. This consistent ability to exceed expectations and the company’s strategic AI initiatives and improve profitability metrics supports the case for a potentially undervalued position.

Investors should consider this favorable PEG ratio alongside Twilio’s market position and growth trajectory. The lower PEG ratio suggests that the market may not be fully pricing in Twilio’s growth prospects, potentially offering an opportunity for investors who believe in the company’s long-term potential in the evolving communications API and enterprise AI landscape.

Is Twilio a Buy or Sell?

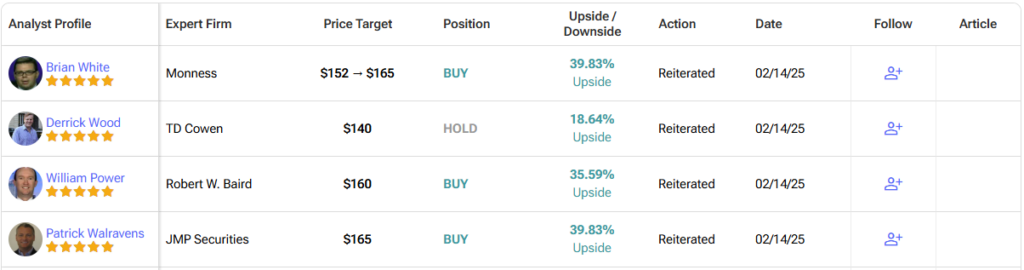

On Wall Street, TWLO stock carries a Moderate Buy consensus rating based on 15 Buy, six Hold, and two Sell ratings obtained over the past three months. TWLO’s average price target of $147.23 per share implies approximately 25% upside potential over the next twelve months.

Twilio’s Pullback May Be an Opportunity

I’m bullish on Twilio, believing the post-earnings selloff is an overreaction. The company’s first-ever GAAP operating profit, strong revenue growth, and improving margins highlight operational strength. Twilio’s AI-driven innovations, such as conversational apps and compliance tools, enhance its product offering and growth prospects. With a compelling PEG ratio below sector averages and robust free cash flow projections, Twilio’s valuation appears attractive. Analyst sentiment remains constructive, supporting the view that this pullback presents an appealing entry point.