3M (MMM) had a remarkable turnaround in 2024, achieving outsized gains that reignited investor confidence. The stock has almost doubled since its 2023 lows, driven by management’s focused efforts to resolve longstanding challenges. Key milestones included the spin-off of its Healthcare Business Group, now rebranded as Solventum (SOLV), and the resolution of two major legal cases. Additionally, 3M implemented the most extensive restructuring program in its history to reduce complexity and improve margins.

While these accomplishments were pivotal to the company’s recovery, I believe the “easy gains” have already been realized. Therefore, I am neutral on MMM stock and recommend a Hold rating.

From a Caterpillar to a Butterfly in 2024

In case you haven’t been keeping up with 3M lately and need a quick recap, the company underwent transformative changes in 2024 that were pivotal to its recovery. A notable move was the spin-off of its Healthcare business, now listed as Solventum. Now, management can sharpen its focus on core industrial, safety, and consumer markets while still realizing the capital benefits of the secondary listing.

At the same time, 3M reached settlements for two high-profile legal issues. One settlement addressed issues related to PFAS chemicals, while the other involved the infamous Combat Arms earplugs lawsuit. These agreements were crucial in offering the clarity Wall Street desperately needed, removing the substantial uncertainty that weighed heavily on the company’s stock price in recent years.

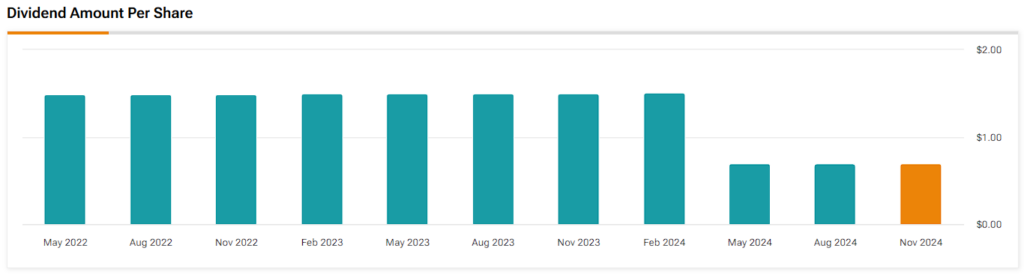

Additionally, 3M executed a considerable restructuring initiative to simplify its complex business model and improve internal efficiencies. Notably, this restructuring effort was the largest in 3M’s history and focused on reducing complexity across all divisions. Assuming all goes well, we should see margins expand in the near to medium term. However, this transformation came with compromises, including a dividend cut that ended 3M’s long-standing status as a Dividend King. Specifically, 3M boasted 66 years of consecutive dividend increases before last year’s dividend cut. Thus, although necessary, the cut certainly disappointed its long-term income-focused investors.

Mediocre Results Translate to Mediocre Share Price Outlook for 3M

While 3M’s much-needed moves to turn around investor sentiment have certainly paid off, its Q4 results reminded us of the limitations of such a mature business. The numbers were decent overall, but nothing really stood out. Specifically, sales came in at $6 billion, marking a slight boost of 0.1% year-over-year, with adjusted sales of $5.8 billion, reflecting 2.1% organic growth. In particular, 3M saw strong demand for products like e-bonding and personal safety equipment. Yet, these gains across all business groups were in tiny chunks.

Regarding profitability, 3M’s results were also average. Adjusted EPS of $1.68 was down 2% year-over-year, with the operating income margin – almost identical to the previous year. Restructuring initiatives helped full-year adjusted EPS grow by 21% to $7.30, with 3M’s results improving significantly in the first half of the year compared to the first half of 2023. Nevertheless, this result was underwhelming in the eyes of analysts and below the historical average. For context, adjusted EPS was assuredly higher at ~$10 since 2021.

Elevated Stock Valuation Limits Further Upside

Following 3M’s share price recovery, its current valuation suggests that most easy gains have already been priced in. To illustrate, for 2025, Wall Street expects the company to achieve an adjusted EPS of $7.80, implying a modest year-over-year growth of about 7%. Analysts then project mid-single-digit growth for the coming years, driven by modest organic growth and some margin expansion as the benefits from the recent restructuring kick in. However, this growth trajectory doesn’t justify paying 19 times this year’s expected earnings, especially in today’s environment.

To clarify, given that interest rates remain relatively high, I would require a P/E ratio closer to 12-14x to be willing to go long on 3M stock, assuming the company delivers mid-single-digit growth over the medium term.

One could argue that 3M has historically traded at a premium valuation, which may hold up. That said, with the company losing its Dividend King status after last year’s dividend cut, there is no reason investors should assign a premium multiple at this time. This is particularly true today, as the post-cut yield of 2% should be far too low to attract income-focused investors who might have been willing to pay a premium for a higher yield from a dividend powerhouse in the past.

Is 3M a Buy or Sell?

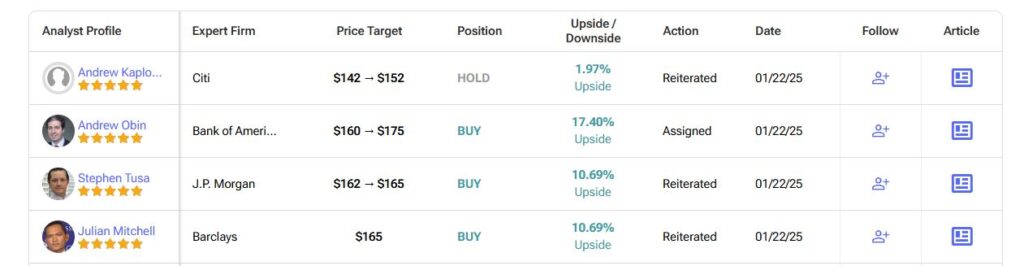

From my perspective, the simple answer is neither because I currently rate 3M as a Hold. Wall Street analysts seem relatively optimistic about 3M stock, however. The safety and industrial, transportation, and electronics conglomerate has gathered seven Buy, three Hold, and two Sell ratings over the past three months, resulting in a Moderate Buy consensus rating. MMM stock currently carries an average price target of $155.75, which implies almost 5% upside potential from current price levels.

3M Revival Set to Fade

In summary, 3M has had a successful financial year, reaching important milestones that have helped its share price rebound. However, there is limited room for further gains following the recent re-rating. Undoubtedly, the company’s restructuring efforts and general operational efficiencies should provide a solid foundation for earnings growth moving forward. Then again, a mid-single-digit earnings growth rate can’t possibly justify the current multiple. For this reason, I have decided to stay on the sidelines on this one.