3M Co. (MMM) is working with advisers on the sale of its food safety business, reports Bloomberg, citing people with knowledge of the matter.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

According to one of the sources, the unit, which sells test kits and other products to help foodmakers monitor sanitation and allergens, could fetch about $3.5 billion.

No final decision has been made and 3M could still decide to keep the business, Bloomberg reported.

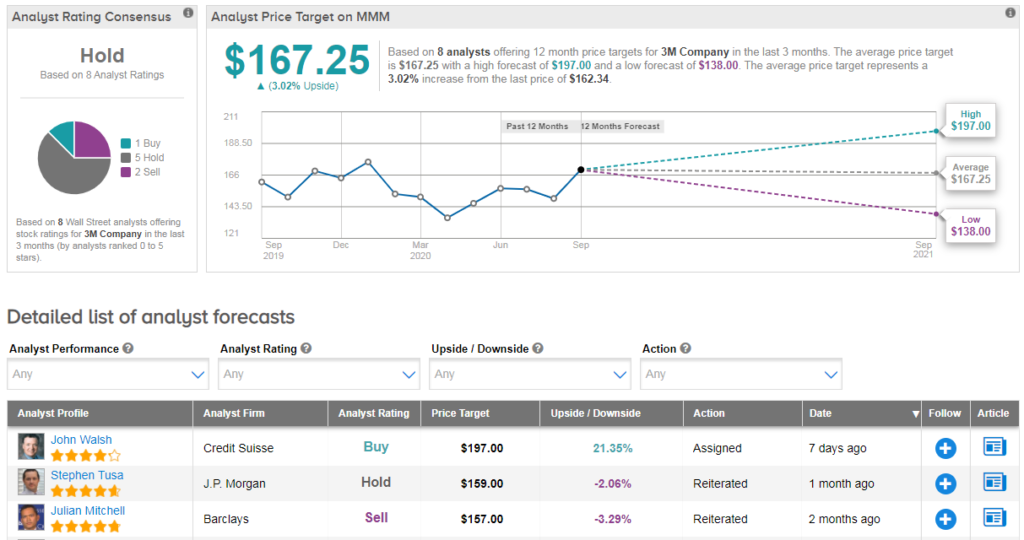

Shares in 3M are down 8% year-to-date, and the stock scores a cautious Hold consensus from the Street. That’s with 5 hold ratings offset by just 1 buy rating and 2 sell ratings in the last three months.

Meanwhile the average analyst price target of $167 suggests only limited upside potential of 3% from the current share price.

On 16 September, lone bull John Walsh of Credit Suisse reiterated his buy rating while ramping up his price target from $179 to $197 (21% upside potential). He also boosted estimates to account for better-than-expected sales performance in July and August.

In August, 3M saw continued stabilization in its monthly organic sales growth rate (+3% y/y adjusted for days). Walsh sees this momentum continuing into 2021 driven by China, automotive production, and semiconductor/ consumer electronics.

“While it is unclear if the company will reinstate guidance on Q3 earnings, we expect 3M to provide guidance once markets stabilize” he stated.

Crucially, the analyst notes that 3M currently trades at a 35% discount to short-cycle peers ITW and ROK. At peer valuation, this equates to $58B of “missing” market value, says Walsh, adding that he expects this discount to erode as 3M rebuilds investor credibility. (See MMM stock analysis on TipRanks).

Related News:

AutoZone’s 4Q Earnings Top Estimates, Analysts See Strong Upside Ahead

Illumina Confirms $8B Acquisition Of Cancer-Detection Firm Grail

Trump Says TikTok Deal To Pass On ‘Zero Security Risk’ Condition – Report